core

¶

angle(ts, threshold=0.01, loss_func='re')

¶

求时间序列ts拟合直线相对于x轴的夹角的余弦值

本函数可以用来判断时间序列的增长趋势。当angle处于[-1, 0]时,越靠近0,下降越快;当angle

处于[0, 1]时,越接近0,上升越快。

如果ts无法很好地拟合为直线,则返回[float, None]

Examples:

>>> ts = np.array([ i for i in range(5)])

>>> round(angle(ts)[1], 3) # degree: 45, rad: pi/2

0.707

>>> ts = np.array([ np.sqrt(3) / 3 * i for i in range(10)])

>>> round(angle(ts)[1],3) # degree: 30, rad: pi/6

0.866

>>> ts = np.array([ -np.sqrt(3) / 3 * i for i in range(7)])

>>> round(angle(ts)[1], 3) # degree: 150, rad: 5*pi/6

-0.866

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

required |

Returns:

| Type | Description |

|---|---|

Tuple[float, float] |

返回 (error, consine(theta)),即拟合误差和夹角余弦值。 |

Source code in omicron/talib/core.py

def angle(ts, threshold=0.01, loss_func="re") -> Tuple[float, float]:

"""求时间序列`ts`拟合直线相对于`x`轴的夹角的余弦值

本函数可以用来判断时间序列的增长趋势。当`angle`处于[-1, 0]时,越靠近0,下降越快;当`angle`

处于[0, 1]时,越接近0,上升越快。

如果`ts`无法很好地拟合为直线,则返回[float, None]

Examples:

>>> ts = np.array([ i for i in range(5)])

>>> round(angle(ts)[1], 3) # degree: 45, rad: pi/2

0.707

>>> ts = np.array([ np.sqrt(3) / 3 * i for i in range(10)])

>>> round(angle(ts)[1],3) # degree: 30, rad: pi/6

0.866

>>> ts = np.array([ -np.sqrt(3) / 3 * i for i in range(7)])

>>> round(angle(ts)[1], 3) # degree: 150, rad: 5*pi/6

-0.866

Args:

ts:

Returns:

返回 (error, consine(theta)),即拟合误差和夹角余弦值。

"""

err, (a, b) = polyfit(ts, deg=1, loss_func=loss_func)

if err > threshold:

return (err, None)

v = np.array([1, a + b])

vx = np.array([1, 0])

return err, copysign(np.dot(v, vx) / (norm(v) * norm(vx)), a)

clustering(numbers, n)

¶

将数组numbers划分为n个簇

返回值为一个List, 每一个元素为一个列表,分别为簇的起始点和长度。

Examples:

>>> numbers = np.array([1,1,1,2,4,6,8,7,4,5,6])

>>> clustering(numbers, 2)

[(0, 4), (4, 7)]

Returns:

| Type | Description |

|---|---|

List[Tuple[int, int]] |

划分后的簇列表。 |

Source code in omicron/talib/core.py

def clustering(numbers: np.ndarray, n: int) -> List[Tuple[int, int]]:

"""将数组`numbers`划分为`n`个簇

返回值为一个List, 每一个元素为一个列表,分别为簇的起始点和长度。

Examples:

>>> numbers = np.array([1,1,1,2,4,6,8,7,4,5,6])

>>> clustering(numbers, 2)

[(0, 4), (4, 7)]

Returns:

划分后的簇列表。

"""

result = ckwrap.cksegs(numbers, n)

clusters = []

for pos, size in zip(result.centers, result.sizes):

clusters.append((int(pos - size // 2 - 1), int(size)))

return clusters

exp_moving_average(values, window)

¶

Numpy implementation of EMA

Source code in omicron/talib/core.py

def exp_moving_average(values, window):

"""Numpy implementation of EMA"""

weights = np.exp(np.linspace(-1.0, 0.0, window))

weights /= weights.sum()

a = np.convolve(values, weights, mode="full")[: len(values)]

a[:window] = a[window]

return a

mean_absolute_error(y, y_hat)

¶

返回预测序列相对于真值序列的平均绝对值差

两个序列应该具有相同的长度。如果存在nan,则nan的值不计入平均值。

Examples:

>>> y = np.arange(5)

>>> y_hat = np.arange(5)

>>> y_hat[4] = 0

>>> mean_absolute_error(y, y)

0.0

>>> mean_absolute_error(y, y_hat)

0.8

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

y |

np.array |

真值序列 |

required |

y_hat |

<built-in function array> |

比较序列 |

required |

Returns:

| Type | Description |

|---|---|

float |

平均绝对值差 |

Source code in omicron/talib/core.py

def mean_absolute_error(y: np.array, y_hat: np.array) -> float:

"""返回预测序列相对于真值序列的平均绝对值差

两个序列应该具有相同的长度。如果存在nan,则nan的值不计入平均值。

Examples:

>>> y = np.arange(5)

>>> y_hat = np.arange(5)

>>> y_hat[4] = 0

>>> mean_absolute_error(y, y)

0.0

>>> mean_absolute_error(y, y_hat)

0.8

Args:

y (np.array): 真值序列

y_hat: 比较序列

Returns:

float: 平均绝对值差

"""

return nanmean(np.abs(y - y_hat))

moving_average(ts, win, padding=True)

¶

生成ts序列的移动平均值

Examples:

>>> ts = np.arange(7)

>>> moving_average(ts, 5)

array([nan, nan, nan, nan, 2., 3., 4.])

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

Sequence |

the input array |

required |

win |

int |

the window size |

required |

padding |

if True, then the return will be equal length as input, padding with np.NaN at the beginning |

True |

Returns:

| Type | Description |

|---|---|

ndarray |

The moving mean of the input array along the specified axis. The output has the same shape as the input. |

Source code in omicron/talib/core.py

def moving_average(ts: Sequence, win: int, padding=True) -> np.ndarray:

"""生成ts序列的移动平均值

Examples:

>>> ts = np.arange(7)

>>> moving_average(ts, 5)

array([nan, nan, nan, nan, 2., 3., 4.])

Args:

ts (Sequence): the input array

win (int): the window size

padding: if True, then the return will be equal length as input, padding with np.NaN at the beginning

Returns:

The moving mean of the input array along the specified axis. The output has the same shape as the input.

"""

ma = move_mean(ts, win)

if padding:

return ma

else:

return ma[win - 1 :]

normalize(X, scaler='maxabs')

¶

对数据进行规范化处理。

如果scaler为maxabs,则X的各元素被压缩到[-1,1]之间 如果scaler为unit_vector,则将X的各元素压缩到单位范数 如果scaler为minmax,则X的各元素被压缩到[0,1]之间 如果scaler为standard,则X的各元素被压缩到单位方差之间,且均值为零。

参考 sklearn

Examples:

>>> X = [[ 1., -1., 2.],

... [ 2., 0., 0.],

... [ 0., 1., -1.]]

>>> expected = [[ 0.4082, -0.4082, 0.8165],

... [ 1., 0., 0.],

... [ 0., 0.7071, -0.7071]]

>>> X_hat = normalize(X, scaler='unit_vector')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal=4)

>>> expected = [[0.5, -1., 1.],

... [1., 0., 0.],

... [0., 1., -0.5]]

>>> X_hat = normalize(X, scaler='maxabs')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal = 2)

>>> expected = [[0.5 , 0. , 1. ],

... [1. , 0.5 , 0.33333333],

... [0. , 1. , 0. ]]

>>> X_hat = normalize(X, scaler='minmax')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal= 3)

>>> X = [[0, 0],

... [0, 0],

... [1, 1],

... [1, 1]]

>>> expected = [[-1., -1.],

... [-1., -1.],

... [ 1., 1.],

... [ 1., 1.]]

>>> X_hat = normalize(X, scaler='standard')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal = 3)

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

X |

2D array |

required | |

scaler |

str |

[description]. Defaults to 'maxabs_scale'. |

'maxabs' |

Source code in omicron/talib/core.py

def normalize(X, scaler="maxabs"):

"""对数据进行规范化处理。

如果scaler为maxabs,则X的各元素被压缩到[-1,1]之间

如果scaler为unit_vector,则将X的各元素压缩到单位范数

如果scaler为minmax,则X的各元素被压缩到[0,1]之间

如果scaler为standard,则X的各元素被压缩到单位方差之间,且均值为零。

参考 [sklearn]

[sklearn]: https://scikit-learn.org/stable/auto_examples/preprocessing/plot_all_scaling.html#results

Examples:

>>> X = [[ 1., -1., 2.],

... [ 2., 0., 0.],

... [ 0., 1., -1.]]

>>> expected = [[ 0.4082, -0.4082, 0.8165],

... [ 1., 0., 0.],

... [ 0., 0.7071, -0.7071]]

>>> X_hat = normalize(X, scaler='unit_vector')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal=4)

>>> expected = [[0.5, -1., 1.],

... [1., 0., 0.],

... [0., 1., -0.5]]

>>> X_hat = normalize(X, scaler='maxabs')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal = 2)

>>> expected = [[0.5 , 0. , 1. ],

... [1. , 0.5 , 0.33333333],

... [0. , 1. , 0. ]]

>>> X_hat = normalize(X, scaler='minmax')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal= 3)

>>> X = [[0, 0],

... [0, 0],

... [1, 1],

... [1, 1]]

>>> expected = [[-1., -1.],

... [-1., -1.],

... [ 1., 1.],

... [ 1., 1.]]

>>> X_hat = normalize(X, scaler='standard')

>>> np.testing.assert_array_almost_equal(expected, X_hat, decimal = 3)

Args:

X (2D array):

scaler (str, optional): [description]. Defaults to 'maxabs_scale'.

"""

if scaler == "maxabs":

return MaxAbsScaler().fit_transform(X)

elif scaler == "unit_vector":

return sklearn.preprocessing.normalize(X, norm="l2")

elif scaler == "minmax":

return minmax_scale(X)

elif scaler == "standard":

return StandardScaler().fit_transform(X)

pct_error(y, y_hat)

¶

相对于序列算术均值的误差值

Examples:

>>> y = np.arange(5)

>>> y_hat = np.arange(5)

>>> y_hat[4] = 0

>>> pct_error(y, y_hat)

0.4

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

y |

np.array |

[description] |

required |

y_hat |

np.array |

[description] |

required |

Returns:

| Type | Description |

|---|---|

float |

[description] |

Source code in omicron/talib/core.py

def pct_error(y: np.array, y_hat: np.array) -> float:

"""相对于序列算术均值的误差值

Examples:

>>> y = np.arange(5)

>>> y_hat = np.arange(5)

>>> y_hat[4] = 0

>>> pct_error(y, y_hat)

0.4

Args:

y (np.array): [description]

y_hat (np.array): [description]

Returns:

float: [description]

"""

mae = mean_absolute_error(y, y_hat)

return mae / nanmean(np.abs(y))

polyfit(ts, deg=2, loss_func='re')

¶

对给定的时间序列进行直线/二次曲线拟合。

二次曲线可以拟合到反生反转的行情,如圆弧底、圆弧顶;也可以拟合到上述趋势中的单边走势,即其中一段曲线。对于如长期均线,在一段时间内走势可能呈现为一条直线,故也可用此函数进行直线拟合。

为便于在不同品种、不同的时间之间对误差、系数进行比较,请事先对ts进行归一化。 如果遇到无法拟合的情况(异常),将返回一个非常大的误差,并将其它项置为np.nan

Examples:

>>> ts = [i for i in range(5)]

>>> err, (a, b) = polyfit(ts, deg=1)

>>> print(round(err, 3), round(a, 1))

0.0 1.0

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

Sequence |

待拟合的时间序列 |

required |

deg |

int |

如果要进行直线拟合,取1;二次曲线拟合取2. Defaults to 2 |

2 |

loss_func |

str |

误差计算方法,取值为 |

're' |

Returns:

| Type | Description |

|---|---|

[Tuple] |

如果为直线拟合,返回误差,(a,b)(一次项系数和常数)。如果为二次曲线拟合,返回 误差, (a,b,c)(二次项、一次项和常量), (vert_x, vert_y)(顶点处的index,顶点值) |

Source code in omicron/talib/core.py

def polyfit(ts: Sequence, deg: int = 2, loss_func="re") -> Tuple:

"""对给定的时间序列进行直线/二次曲线拟合。

二次曲线可以拟合到反生反转的行情,如圆弧底、圆弧顶;也可以拟合到上述趋势中的单边走势,即其中一段曲线。对于如长期均线,在一段时间内走势可能呈现为一条直线,故也可用此函数进行直线拟合。

为便于在不同品种、不同的时间之间对误差、系数进行比较,请事先对ts进行归一化。

如果遇到无法拟合的情况(异常),将返回一个非常大的误差,并将其它项置为np.nan

Examples:

>>> ts = [i for i in range(5)]

>>> err, (a, b) = polyfit(ts, deg=1)

>>> print(round(err, 3), round(a, 1))

0.0 1.0

Args:

ts (Sequence): 待拟合的时间序列

deg (int): 如果要进行直线拟合,取1;二次曲线拟合取2. Defaults to 2

loss_func (str): 误差计算方法,取值为`mae`, `rmse`,`mse` 或`re`。Defaults to `re` (relative_error)

Returns:

[Tuple]: 如果为直线拟合,返回误差,(a,b)(一次项系数和常数)。如果为二次曲线拟合,返回

误差, (a,b,c)(二次项、一次项和常量), (vert_x, vert_y)(顶点处的index,顶点值)

"""

if deg not in (1, 2):

raise ValueError("deg must be 1 or 2")

try:

if any(np.isnan(ts)):

raise ValueError("ts contains nan")

x = np.array(list(range(len(ts))))

z = np.polyfit(x, ts, deg=deg)

p = np.poly1d(z)

ts_hat = np.array([p(xi) for xi in x])

if loss_func == "mse":

error = np.mean(np.square(ts - ts_hat))

elif loss_func == "rmse":

error = np.sqrt(np.mean(np.square(ts - ts_hat)))

elif loss_func == "mae":

error = mean_absolute_error(ts, ts_hat)

else: # defaults to relative error

error = pct_error(ts, ts_hat)

if deg == 2:

a, b, c = z[0], z[1], z[2]

axis_x = -b / (2 * a)

if a != 0:

axis_y = (4 * a * c - b * b) / (4 * a)

else:

axis_y = None

return error, z, (axis_x, axis_y)

elif deg == 1:

return error, z

except Exception:

error = 1e9

if deg == 1:

return error, (np.nan, np.nan)

else:

return error, (np.nan, np.nan, np.nan), (np.nan, np.nan)

slope(ts, loss_func='re')

¶

求ts表示的直线(如果能拟合成直线的话)的斜率

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.array |

[description] |

required |

loss_func |

str |

[description]. Defaults to 're'. |

're' |

Source code in omicron/talib/core.py

def slope(ts: np.array, loss_func="re"):

"""求ts表示的直线(如果能拟合成直线的话)的斜率

Args:

ts (np.array): [description]

loss_func (str, optional): [description]. Defaults to 're'.

"""

err, (a, b) = polyfit(ts, deg=1, loss_func=loss_func)

return err, a

smooth(ts, win, poly_order=1, mode='interp')

¶

平滑序列ts,使用窗口大小为win的平滑模型,默认使用线性模型

提供本函数主要基于这样的考虑: omicron的使用者可能并不熟悉信号处理的概念,这里相当于提供了相关功能的一个入口。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.array |

[description] |

required |

win |

int |

[description] |

required |

poly_order |

int |

[description]. Defaults to 1. |

1 |

Source code in omicron/talib/core.py

def smooth(ts: np.array, win: int, poly_order=1, mode="interp"):

"""平滑序列ts,使用窗口大小为win的平滑模型,默认使用线性模型

提供本函数主要基于这样的考虑: omicron的使用者可能并不熟悉信号处理的概念,这里相当于提供了相关功能的一个入口。

Args:

ts (np.array): [description]

win (int): [description]

poly_order (int, optional): [description]. Defaults to 1.

"""

return savgol_filter(ts, win, poly_order, mode=mode)

weighted_moving_average(ts, win)

¶

计算加权移动平均

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.array |

[description] |

required |

win |

int |

[description] |

required |

Returns:

| Type | Description |

|---|---|

np.array |

[description] |

Source code in omicron/talib/core.py

def weighted_moving_average(ts: np.array, win: int) -> np.array:

"""计算加权移动平均

Args:

ts (np.array): [description]

win (int): [description]

Returns:

np.array: [description]

"""

w = [2 * (i + 1) / (win * (win + 1)) for i in range(win)]

return np.convolve(ts, w, "valid")

morph

¶

形态检测相关方法

BreakoutFlag (IntEnum)

¶

An enumeration.

Source code in omicron/talib/morph.py

class BreakoutFlag(IntEnum):

UP = 1

DOWN = -1

NONE = 0

CrossFlag (IntEnum)

¶

An enumeration.

Source code in omicron/talib/morph.py

class CrossFlag(IntEnum):

UPCROSS = 1

DOWNCROSS = -1

NONE = 0

breakout(ts, upthres=0.01, downthres=-0.01, confirm=1)

¶

检测时间序列是否突破了压力线(整理线)

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.ndarray |

时间序列 |

required |

upthres |

float |

0.01 |

|

downthres |

float |

-0.01 |

|

confirm |

int |

经过多少个bars后,才确认突破。默认为1 |

1 |

Returns:

| Type | Description |

|---|---|

BreakoutFlag |

如果上向突破压力线,返回1,如果向下突破压力线,返回-1,否则返回0 |

Source code in omicron/talib/morph.py

def breakout(

ts: np.ndarray, upthres: float = 0.01, downthres: float = -0.01, confirm: int = 1

) -> BreakoutFlag:

"""检测时间序列是否突破了压力线(整理线)

Args:

ts (np.ndarray): 时间序列

upthres (float, optional): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

downthres (float, optional): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

confirm (int, optional): 经过多少个bars后,才确认突破。默认为1

Returns:

如果上向突破压力线,返回1,如果向下突破压力线,返回-1,否则返回0

"""

support, resist, _ = support_resist_lines(ts[:-confirm], upthres, downthres)

x0 = len(ts) - confirm - 1

x = list(range(len(ts) - confirm, len(ts)))

if resist is not None:

if np.all(ts[x] > resist(x)) and ts[x0] <= resist(x0):

return BreakoutFlag.UP

if support is not None:

if np.all(ts[x] < support(x)) and ts[x0] >= support(x0):

return BreakoutFlag.DOWN

return BreakoutFlag.NONE

cross(f, g)

¶

判断序列f是否与g相交。如果两个序列有且仅有一个交点,则返回1表明f上交g;-1表明f下交g

本方法可用以判断两条均线是否相交。

Returns:

| Type | Description |

|---|---|

CrossFlag |

(flag, index), 其中flag取值为: 0 无效 -1 f向下交叉g 1 f向上交叉g |

Source code in omicron/talib/morph.py

def cross(f: np.ndarray, g: np.ndarray) -> CrossFlag:

"""判断序列f是否与g相交。如果两个序列有且仅有一个交点,则返回1表明f上交g;-1表明f下交g

本方法可用以判断两条均线是否相交。

returns:

(flag, index), 其中flag取值为:

0 无效

-1 f向下交叉g

1 f向上交叉g

"""

indices = np.argwhere(np.diff(np.sign(f - g))).flatten()

if len(indices) == 0:

return CrossFlag.NONE, 0

# 如果存在一个或者多个交点,取最后一个

idx = indices[-1]

if f[idx] < g[idx]:

return CrossFlag.UPCROSS, idx

elif f[idx] > g[idx]:

return CrossFlag.DOWNCROSS, idx

else:

return CrossFlag(np.sign(g[idx - 1] - f[idx - 1])), idx

energy_hump(bars, thresh=2)

¶

检测bars中是否存在两波以上量能剧烈增加的情形(能量驼峰),返回最后一波距现在的位置及区间长度。

注意如果最后一个能量驼峰距现在过远(比如超过10个bar),可能意味着资金已经逃离,能量已经耗尽。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

bars |

[('frame', '<M8[s]'), ('open', '<f4'), ('high', '<f4'), ('low', '<f4'), ('close', '<f4'), ('volume', '<f8'), ('amount', '<f8'), ('factor', '<f4')] |

行情数据 |

required |

thresh |

最后一波量必须大于20天均量的倍数。 |

2 |

Returns:

| Type | Description |

|---|---|

Optional[Tuple[int, int]] |

如果不存在能量驼峰的情形,则返回None,否则返回最后一个驼峰离现在的距离及区间长度。 |

Source code in omicron/talib/morph.py

def energy_hump(bars: bars_dtype, thresh=2) -> Optional[Tuple[int, int]]:

"""检测`bars`中是否存在两波以上量能剧烈增加的情形(能量驼峰),返回最后一波距现在的位置及区间长度。

注意如果最后一个能量驼峰距现在过远(比如超过10个bar),可能意味着资金已经逃离,能量已经耗尽。

Args:

bars: 行情数据

thresh: 最后一波量必须大于20天均量的倍数。

Returns:

如果不存在能量驼峰的情形,则返回None,否则返回最后一个驼峰离现在的距离及区间长度。

"""

vol = bars["volume"]

std = np.std(vol[1:] / vol[:-1])

pvs = peak_valley_pivots(vol, std, 0)

frames = bars["frame"]

pvs[0] = 0

pvs[-1] = -1

peaks = np.argwhere(pvs == 1)

mn = np.mean(vol[peaks])

# 顶点不能缩量到尖峰均值以下

real_peaks = np.intersect1d(np.argwhere(vol > mn), peaks)

if len(real_peaks) < 2:

return None

logger.debug("found %s peaks at %s", len(real_peaks), frames[real_peaks])

lp = real_peaks[-1]

ma = moving_average(vol, 20)[lp]

if vol[lp] < ma * thresh:

logger.debug(

"vol of last peak[%s] is less than mean_vol(20) * thresh[%s]",

vol[lp],

ma * thresh,

)

return None

return len(bars) - real_peaks[-1], real_peaks[-1] - real_peaks[0]

inverse_vcross(f, g)

¶

判断序列f是否与序列g存在^型相交。即存在两个交点,第一个交点为向上相交,第二个交点为向下 相交。可用于判断见顶特征等场合。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

f |

np.array |

[description] |

required |

g |

np.array |

[description] |

required |

Returns:

| Type | Description |

|---|---|

Tuple |

[description] |

Source code in omicron/talib/morph.py

def inverse_vcross(f: np.array, g: np.array) -> Tuple:

"""判断序列f是否与序列g存在^型相交。即存在两个交点,第一个交点为向上相交,第二个交点为向下

相交。可用于判断见顶特征等场合。

Args:

f (np.array): [description]

g (np.array): [description]

Returns:

Tuple: [description]

"""

indices = np.argwhere(np.diff(np.sign(f - g))).flatten()

if len(indices) == 2:

idx0, idx1 = indices

if f[idx0] < g[idx0] and f[idx1] > g[idx1]:

return True, (idx0, idx1)

return False, (None, None)

peaks_and_valleys(ts, up_thresh=None, down_thresh=None)

¶

寻找ts中的波峰和波谷,返回数组指示在该位置上是否为波峰或波谷。如果为1,则为波峰;如果为-1,则为波谷。

本函数直接使用了zigzag中的peak_valley_pivots. 有很多方法可以实现本功能,比如scipy.signals.find_peaks_cwt, peak_valley_pivots等。本函数更适合金融时间序列,并且使用了cython加速。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.ndarray |

时间序列 |

required |

up_thresh |

float |

波峰的阈值,如果为None,则使用ts变化率的二倍标准差 |

None |

down_thresh |

float |

波谷的阈值,如果为None,则使用ts变化率的二倍标准差乘以-1 |

None |

Returns:

| Type | Description |

|---|---|

np.ndarray |

返回数组指示在该位置上是否为波峰或波谷。 |

Source code in omicron/talib/morph.py

def peaks_and_valleys(

ts: np.ndarray,

up_thresh: Optional[float] = None,

down_thresh: Optional[float] = None,

) -> np.ndarray:

"""寻找ts中的波峰和波谷,返回数组指示在该位置上是否为波峰或波谷。如果为1,则为波峰;如果为-1,则为波谷。

本函数直接使用了zigzag中的peak_valley_pivots. 有很多方法可以实现本功能,比如scipy.signals.find_peaks_cwt, peak_valley_pivots等。本函数更适合金融时间序列,并且使用了cython加速。

Args:

ts (np.ndarray): 时间序列

up_thresh (float): 波峰的阈值,如果为None,则使用ts变化率的二倍标准差

down_thresh (float): 波谷的阈值,如果为None,则使用ts变化率的二倍标准差乘以-1

Returns:

np.ndarray: 返回数组指示在该位置上是否为波峰或波谷。

"""

if ts.dtype != np.float64:

ts = ts.astype(np.float64)

if any([up_thresh is None, down_thresh is None]):

change_rate = ts[1:] / ts[:-1] - 1

std = np.std(change_rate)

up_thresh = up_thresh or 2 * std

down_thresh = down_thresh or -2 * std

return peak_valley_pivots(ts, up_thresh, down_thresh)

plateaus(numbers, min_size, fall_in_range_ratio=0.97)

¶

统计数组numbers中的可能存在的平台整理。

如果一个数组中存在着子数组,使得其元素与均值的距离落在三个标准差以内的比例超过fall_in_range_ratio的,则认为该子数组满足平台整理。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

numbers |

ndarray |

输入数组 |

required |

min_size |

int |

平台的最小长度 |

required |

fall_in_range_ratio |

float |

超过 |

0.97 |

Returns:

| Type | Description |

|---|---|

List[Tuple] |

平台的起始位置和长度的数组 |

Source code in omicron/talib/morph.py

def plateaus(

numbers: np.ndarray, min_size: int, fall_in_range_ratio: float = 0.97

) -> List[Tuple]:

"""统计数组`numbers`中的可能存在的平台整理。

如果一个数组中存在着子数组,使得其元素与均值的距离落在三个标准差以内的比例超过`fall_in_range_ratio`的,则认为该子数组满足平台整理。

Args:

numbers: 输入数组

min_size: 平台的最小长度

fall_in_range_ratio: 超过`fall_in_range_ratio`比例的元素落在均值的三个标准差以内,就认为该子数组构成一个平台

Returns:

平台的起始位置和长度的数组

"""

if numbers.size <= min_size:

n = 1

else:

n = numbers.size // min_size

clusters = clustering(numbers, n)

plats = []

for (start, length) in clusters:

if length < min_size:

continue

y = numbers[start : start + length]

mean = np.mean(y)

std = np.std(y)

inrange = len(y[np.abs(y - mean) < 3 * std])

ratio = inrange / length

if ratio >= fall_in_range_ratio:

plats.append((start, length))

return plats

rsi_bottom_distance(close, thresh=None)

¶

根据给定的收盘价,计算最后一个数据到上一个发出rsi低水平的距离, 如果从上一个最低点rsi到最后一个数据并未发出低水平信号, 返回最后一个数据到上一个发出最低点rsi的距离。

其中close的长度一般不小于60。 返回值为距离整数,不满足条件则返回None。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.array |

具有时间序列的收盘价 |

required |

thresh |

Tuple[float, float]) |

None适用所有股票,不必更改,也可自行设置。 |

None |

Returns:

| Type | Description |

|---|---|

int |

返回最后一个数据到上一个发出rsi低水平的距离。 如果从上一个最低点rsi到最后一个数据并未发出低水平信号, 返回最后一个数据到上一个发出最低点rsi的距离。 除此之外,返回None。 |

Source code in omicron/talib/morph.py

def rsi_bottom_distance(close: np.array, thresh: Tuple[float, float] = None) -> int:

"""根据给定的收盘价,计算最后一个数据到上一个发出rsi低水平的距离,

如果从上一个最低点rsi到最后一个数据并未发出低水平信号,

返回最后一个数据到上一个发出最低点rsi的距离。

其中close的长度一般不小于60。

返回值为距离整数,不满足条件则返回None。

Args:

close (np.array): 具有时间序列的收盘价

thresh (Tuple[float, float]) : None适用所有股票,不必更改,也可自行设置。

Returns:

返回最后一个数据到上一个发出rsi低水平的距离。

如果从上一个最低点rsi到最后一个数据并未发出低水平信号,

返回最后一个数据到上一个发出最低点rsi的距离。

除此之外,返回None。"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if close.dtype != np.float64:

close = close.astype(np.float64)

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

rsi = ta.RSI(close, 6)

watermarks = rsi_watermarks(close, thresh)

if watermarks is not None:

low_watermark, _, _ = watermarks

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

pivots[0], pivots[-1] = 0, 0

# 谷值RSI<30

valley_rsi_index = np.where((rsi < 30) & (pivots == -1))[0]

# RSI低水平的最大值:低水平*1.01

low_rsi_index = np.where(rsi <= low_watermark * 1.01)[0]

if len(valley_rsi_index) > 0:

distance = len(rsi) - 1 - valley_rsi_index[-1]

if len(low_rsi_index) > 0:

if low_rsi_index[-1] >= valley_rsi_index[-1]:

distance = len(rsi) - 1 - low_rsi_index[-1]

return distance

rsi_bottom_divergent(close, thresh=None, rsi_limit=30)

¶

寻找最近满足条件的rsi底背离。

返回最后一个数据到最近底背离发生点的距离;没有满足条件的底背离,返回None。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.array |

时间序列收盘价 |

required |

thresh |

Tuple[float, float] |

None |

|

rsi_limit |

float |

RSI发生底背离时的阈值, 默认值30(20效果更佳,但是检测出来数量太少),即只过滤RSI6<30的局部最低收盘价。 |

30 |

Returns:

| Type | Description |

|---|---|

int |

返回int类型的整数,表示最后一个数据到最近底背离发生点的距离;没有满足条件的底背离,返回None。 |

Source code in omicron/talib/morph.py

def rsi_bottom_divergent(

close: np.array, thresh: Tuple[float, float] = None, rsi_limit: float = 30

) -> int:

"""寻找最近满足条件的rsi底背离。

返回最后一个数据到最近底背离发生点的距离;没有满足条件的底背离,返回None。

Args:

close (np.array): 时间序列收盘价

thresh (Tuple[float, float]): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

rsi_limit (float, optional): RSI发生底背离时的阈值, 默认值30(20效果更佳,但是检测出来数量太少),即只过滤RSI6<30的局部最低收盘价。

Returns:

返回int类型的整数,表示最后一个数据到最近底背离发生点的距离;没有满足条件的底背离,返回None。

"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if close.dtype != np.float64:

close = close.astype(np.float64)

rsi = ta.RSI(close, 6)

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

pivots[0], pivots[-1] = 0, 0

length = len(close)

valley_index = np.where((pivots == -1) & (rsi <= rsi_limit))[0]

if len(valley_index) >= 2:

if (close[valley_index[-1]] < close[valley_index[-2]]) and (

rsi[valley_index[-1]] > rsi[valley_index[-2]]

):

bottom_dev_distance = length - 1 - valley_index[-1]

return bottom_dev_distance

rsi_predict_price(close, thresh=None)

¶

给定一段行情,根据最近的两个RSI的极小值和极大值预测下一个周期可能达到的最低价格和最高价格。

其原理是,以预测最近的两个最高价和最低价,求出其相对应的RSI值,求出最高价和最低价RSI的均值, 若只有一个则取最近的一个。再由RSI公式,反推价格。此时返回值为(None, float),即只有最高价,没有最低价。反之亦然。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.ndarray |

具有时间序列的收盘价 |

required |

thresh |

Tuple[float, float]) |

None |

Returns:

| Type | Description |

|---|---|

Tuple[float, float] |

返回数组[predicted_low_price, predicted_high_price], 数组第一个值为利用达到之前最低收盘价的RSI预测的最低价。 第二个值为利用达到之前最高收盘价的RSI预测的最高价。 |

Source code in omicron/talib/morph.py

def rsi_predict_price(

close: np.ndarray, thresh: Tuple[float, float] = None

) -> Tuple[float, float]:

"""给定一段行情,根据最近的两个RSI的极小值和极大值预测下一个周期可能达到的最低价格和最高价格。

其原理是,以预测最近的两个最高价和最低价,求出其相对应的RSI值,求出最高价和最低价RSI的均值,

若只有一个则取最近的一个。再由RSI公式,反推价格。此时返回值为(None, float),即只有最高价,没有最低价。反之亦然。

Args:

close (np.ndarray): 具有时间序列的收盘价

thresh (Tuple[float, float]) : 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

Returns:

返回数组[predicted_low_price, predicted_high_price], 数组第一个值为利用达到之前最低收盘价的RSI预测的最低价。

第二个值为利用达到之前最高收盘价的RSI预测的最高价。

"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

if close.dtype != np.float64:

close = close.astype(np.float64)

valley_rsi, peak_rsi, _ = rsi_watermarks(close, thresh=thresh)

pivot = peak_valley_pivots(close, thresh[0], thresh[1])

pivot[0], pivot[-1] = 0, 0 # 掐头去尾

price_change = pd.Series(close).diff(1).values

ave_price_change = (abs(price_change)[-6:].mean()) * 5

ave_price_raise = (np.maximum(price_change, 0)[-6:].mean()) * 5

if valley_rsi is not None:

predicted_low_change = (ave_price_change) - ave_price_raise / (

0.01 * valley_rsi

)

if predicted_low_change > 0:

predicted_low_change = 0

predicted_low_price = close[-1] + predicted_low_change

else:

predicted_low_price = None

if peak_rsi is not None:

predicted_high_change = (ave_price_raise - ave_price_change) / (

0.01 * peak_rsi - 1

) - ave_price_change

if predicted_high_change < 0:

predicted_high_change = 0

predicted_high_price = close[-1] + predicted_high_change

else:

predicted_high_price = None

return predicted_low_price, predicted_high_price

rsi_top_distance(close, thresh=None)

¶

根据给定的收盘价,计算最后一个数据到上一个发出rsi高水平的距离, 如果从上一个最高点rsi到最后一个数据并未发出高水平信号, 返回最后一个数据到上一个发出最高点rsi的距离。

其中close的长度一般不小于60。 返回值为距离整数,不满足条件则返回None。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.array |

具有时间序列的收盘价 |

required |

thresh |

Tuple[float, float]) |

None适用所有股票,不必更改,也可自行设置。 |

None |

Returns:

| Type | Description |

|---|---|

int |

返回最后一个数据到上一个发出rsi高水平的距离。 如果从上一个最高点rsi到最后一个数据并未发出高水平信号, 返回最后一个数据到上一个发出最高点rsi的距离。 除此之外,返回None。 |

Source code in omicron/talib/morph.py

def rsi_top_distance(close: np.array, thresh: Tuple[float, float] = None) -> int:

"""根据给定的收盘价,计算最后一个数据到上一个发出rsi高水平的距离,

如果从上一个最高点rsi到最后一个数据并未发出高水平信号,

返回最后一个数据到上一个发出最高点rsi的距离。

其中close的长度一般不小于60。

返回值为距离整数,不满足条件则返回None。

Args:

close (np.array): 具有时间序列的收盘价

thresh (Tuple[float, float]) : None适用所有股票,不必更改,也可自行设置。

Returns:

返回最后一个数据到上一个发出rsi高水平的距离。

如果从上一个最高点rsi到最后一个数据并未发出高水平信号,

返回最后一个数据到上一个发出最高点rsi的距离。

除此之外,返回None。"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if close.dtype != np.float64:

close = close.astype(np.float64)

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

rsi = ta.RSI(close, 6)

watermarks = rsi_watermarks(close, thresh)

if watermarks is not None:

_, high_watermark, _ = watermarks

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

pivots[0], pivots[-1] = 0, 0

# 峰值RSI>70

peak_rsi_index = np.where((rsi > 70) & (pivots == 1))[0]

# RSI高水平的最小值:高水平*0.99

high_rsi_index = np.where(rsi >= high_watermark * 0.99)[0]

if len(peak_rsi_index) > 0:

distance = len(rsi) - 1 - peak_rsi_index[-1]

if len(high_rsi_index) > 0:

if high_rsi_index[-1] >= peak_rsi_index[-1]:

distance = len(rsi) - 1 - high_rsi_index[-1]

return distance

rsi_top_divergent(close, thresh=None, rsi_limit=70)

¶

寻找最近满足条件的rsi顶背离。

返回最后一个数据到最近顶背离发生点的距离;没有满足条件的顶背离,返回None。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.array |

时间序列收盘价 |

required |

thresh |

Tuple[float, float] |

None |

|

rsi_limit |

float |

RSI发生顶背离时的阈值, 默认值70(80效果更佳,但是检测出来数量太少),即只过滤RSI6>70的局部最高收盘价。 |

70 |

Returns:

| Type | Description |

|---|---|

Tuple[int, int] |

返回int类型的整数,表示最后一个数据到最近顶背离发生点的距离;没有满足条件的顶背离,返回None。 |

Source code in omicron/talib/morph.py

def rsi_top_divergent(

close: np.array, thresh: Tuple[float, float] = None, rsi_limit: float = 70

) -> Tuple[int, int]:

"""寻找最近满足条件的rsi顶背离。

返回最后一个数据到最近顶背离发生点的距离;没有满足条件的顶背离,返回None。

Args:

close (np.array): 时间序列收盘价

thresh (Tuple[float, float]): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

rsi_limit (float, optional): RSI发生顶背离时的阈值, 默认值70(80效果更佳,但是检测出来数量太少),即只过滤RSI6>70的局部最高收盘价。

Returns:

返回int类型的整数,表示最后一个数据到最近顶背离发生点的距离;没有满足条件的顶背离,返回None。

"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if close.dtype != np.float64:

close = close.astype(np.float64)

rsi = ta.RSI(close, 6)

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

pivots[0], pivots[-1] = 0, 0

length = len(close)

peak_index = np.where((pivots == 1) & (rsi >= rsi_limit))[0]

if len(peak_index) >= 2:

if (close[peak_index[-1]] > close[peak_index[-2]]) and (

rsi[peak_index[-1]] < rsi[peak_index[-2]]

):

top_dev_distance = length - 1 - peak_index[-1]

return top_dev_distance

rsi_watermarks(close, thresh=None)

¶

给定一段行情数据和用以检测顶和底的阈值,返回该段行情中,谷和峰处RSI均值,最后一个RSI6值。

其中close的长度一般不小于60,不大于120。返回值中,一个为low_wartermark(谷底处RSI值), 一个为high_wartermark(高峰处RSI值),一个为RSI6的最后一个值,用以对比前两个警戒值。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.array |

具有时间序列的收盘价 |

required |

thresh |

Tuple[float, float]) |

None适用所有股票,不必更改,也可自行设置。 |

None |

Returns:

| Type | Description |

|---|---|

Tuple[float, float, float] |

返回数组[low_watermark, high_watermark, rsi[-1]], 第一个为最近两个最低收盘价的RSI均值, 第二个为最近两个最高收盘价的RSI均值。 若传入收盘价只有一个最值,只返回一个。没有最值,则返回None, 第三个为实际的最后RSI6的值。 |

Source code in omicron/talib/morph.py

def rsi_watermarks(

close: np.array, thresh: Tuple[float, float] = None

) -> Tuple[float, float, float]:

"""给定一段行情数据和用以检测顶和底的阈值,返回该段行情中,谷和峰处RSI均值,最后一个RSI6值。

其中close的长度一般不小于60,不大于120。返回值中,一个为low_wartermark(谷底处RSI值),

一个为high_wartermark(高峰处RSI值),一个为RSI6的最后一个值,用以对比前两个警戒值。

Args:

close (np.array): 具有时间序列的收盘价

thresh (Tuple[float, float]) : None适用所有股票,不必更改,也可自行设置。

Returns:

返回数组[low_watermark, high_watermark, rsi[-1]], 第一个为最近两个最低收盘价的RSI均值, 第二个为最近两个最高收盘价的RSI均值。

若传入收盘价只有一个最值,只返回一个。没有最值,则返回None, 第三个为实际的最后RSI6的值。

"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

if close.dtype != np.float64:

close = close.astype(np.float64)

rsi = ta.RSI(close, 6)

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

pivots[0], pivots[-1] = 0, 0 # 掐头去尾

# 峰值RSI>70; 谷处的RSI<30;

peaks_rsi_index = np.where((rsi > 70) & (pivots == 1))[0]

valleys_rsi_index = np.where((rsi < 30) & (pivots == -1))[0]

if len(peaks_rsi_index) == 0:

high_watermark = None

elif len(peaks_rsi_index) == 1:

high_watermark = rsi[peaks_rsi_index[0]]

else: # 有两个以上的峰,通过最近的两个峰均值来确定走势

high_watermark = np.nanmean(rsi[peaks_rsi_index[-2:]])

if len(valleys_rsi_index) == 0:

low_watermark = None

elif len(valleys_rsi_index) == 1:

low_watermark = rsi[valleys_rsi_index[0]]

else: # 有两个以上的峰,通过最近的两个峰来确定走势

low_watermark = np.nanmean(rsi[valleys_rsi_index[-2:]])

return low_watermark, high_watermark, rsi[-1]

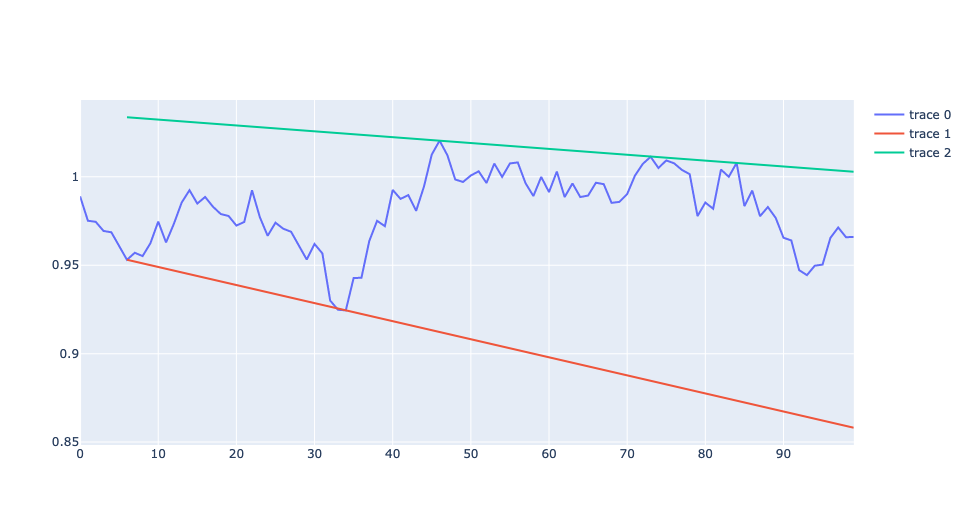

support_resist_lines(ts, upthres=None, downthres=None)

¶

计算时间序列的支撑线和阻力线

使用最近的两个高点连接成阴力线,两个低点连接成支撑线。

Examples:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 | |

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

ts |

np.ndarray |

时间序列 |

required |

upthres |

float |

None |

|

downthres |

float |

None |

Returns:

| Type | Description |

|---|---|

Tuple[Callable, Callable, numpy.ndarray] |

返回支撑线和阻力线的计算函数及起始点坐标,如果没有支撑线或阻力线,则返回None |

Source code in omicron/talib/morph.py

def support_resist_lines(

ts: np.ndarray, upthres: float = None, downthres: float = None

) -> Tuple[Callable, Callable, np.ndarray]:

"""计算时间序列的支撑线和阻力线

使用最近的两个高点连接成阴力线,两个低点连接成支撑线。

Examples:

```python

def show_support_resist_lines(ts):

import plotly.graph_objects as go

fig = go.Figure()

support, resist, x_start = support_resist_lines(ts, 0.03, -0.03)

fig.add_trace(go.Scatter(x=np.arange(len(ts)), y=ts))

x = np.arange(len(ts))[x_start:]

fig.add_trace(go.Line(x=x, y = support(x)))

fig.add_trace(go.Line(x=x, y = resist(x)))

fig.show()

np.random.seed(1978)

X = np.cumprod(1 + np.random.randn(100) * 0.01)

show_support_resist_lines(X)

```

the above code will show this

Args:

ts (np.ndarray): 时间序列

upthres (float, optional): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

downthres (float, optional): 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

Returns:

返回支撑线和阻力线的计算函数及起始点坐标,如果没有支撑线或阻力线,则返回None

"""

if ts.dtype != np.float64:

ts = ts.astype(np.float64)

pivots = peaks_and_valleys(ts, upthres, downthres)

pivots[0] = 0

pivots[-1] = 0

arg_max = np.argwhere(pivots == 1).flatten()

arg_min = np.argwhere(pivots == -1).flatten()

resist = None

support = None

if len(arg_max) >= 2:

arg_max = arg_max[-2:]

y = ts[arg_max]

coeff = np.polyfit(arg_max, y, deg=1)

resist = np.poly1d(coeff)

if len(arg_min) >= 2:

arg_min = arg_min[-2:]

y = ts[arg_min]

coeff = np.polyfit(arg_min, y, deg=1)

support = np.poly1d(coeff)

return support, resist, np.min([*arg_min, *arg_max])

valley_detect(close, thresh=(0.05, -0.02))

¶

给定一段行情数据和用以检测近期已发生反转的最低点,返回该段行情中,最低点到最后一个数据的距离和收益率数组, 如果给定行情中未找到满足参数的最低点,则返回两个空值数组。

其中bars的长度一般不小于60,不大于120。此函数采用了zigzag中的谷峰检测方法,其中参数默认(0.05,-0.02), 此参数对所有股票数据都适用。若满足参数,返回值中,距离为大于0的整数,收益率是0~1的小数。

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

close |

np.ndarray |

具有时间序列的收盘价 |

required |

thresh |

Tuple[float, float]) |

(0.05, -0.02) |

Returns:

| Type | Description |

|---|---|

int |

返回该段行情中,最低点到最后一个数据的距离和收益率数组, 如果给定行情中未找到满足参数的最低点,则返回两个空值数组。 |

Source code in omicron/talib/morph.py

def valley_detect(

close: np.ndarray, thresh: Tuple[float, float] = (0.05, -0.02)

) -> int:

"""给定一段行情数据和用以检测近期已发生反转的最低点,返回该段行情中,最低点到最后一个数据的距离和收益率数组,

如果给定行情中未找到满足参数的最低点,则返回两个空值数组。

其中bars的长度一般不小于60,不大于120。此函数采用了zigzag中的谷峰检测方法,其中参数默认(0.05,-0.02),

此参数对所有股票数据都适用。若满足参数,返回值中,距离为大于0的整数,收益率是0~1的小数。

Args:

close (np.ndarray): 具有时间序列的收盘价

thresh (Tuple[float, float]) : 请参考[peaks_and_valleys][omicron.talib.morph.peaks_and_valleys]

Returns:

返回该段行情中,最低点到最后一个数据的距离和收益率数组,

如果给定行情中未找到满足参数的最低点,则返回两个空值数组。

"""

assert len(close) >= 60, "must provide an array with at least 60 length!"

if close.dtype != np.float64:

close = close.astype(np.float64)

if thresh is None:

std = np.std(close[-59:] / close[-60:-1] - 1)

thresh = (2 * std, -2 * std)

pivots = peak_valley_pivots(close, thresh[0], thresh[1])

flags = pivots[pivots != 0]

increased = None

lowest_distance = None

if (flags[-2] == -1) and (flags[-1] == 1):

length = len(pivots)

valley_index = np.where(pivots == -1)[0]

increased = (close[-1] - close[valley_index[-1]]) / close[valley_index[-1]]

lowest_distance = int(length - 1 - valley_index[-1])

return lowest_distance, increased

vcross(f, g)

¶

判断序列f是否与g存在类型v型的相交。即存在两个交点,第一个交点为向下相交,第二个交点为向上 相交。一般反映为洗盘拉升的特征。

Examples:

>>> f = np.array([ 3 * i ** 2 - 20 * i + 2 for i in range(10)])

>>> g = np.array([ i - 5 for i in range(10)])

>>> flag, indices = vcross(f, g)

>>> assert flag is True

>>> assert indices[0] == 0

>>> assert indices[1] == 6

Parameters:

| Name | Type | Description | Default |

|---|---|---|---|

f |

<built-in function array> |

first sequence |

required |

g |

<built-in function array> |

the second sequence |

required |

Returns:

| Type | Description |

|---|---|

Tuple |

(flag, indices), 其中flag取值为True时,存在vcross,indices为交点的索引。 |

Source code in omicron/talib/morph.py

def vcross(f: np.array, g: np.array) -> Tuple:

"""判断序列f是否与g存在类型v型的相交。即存在两个交点,第一个交点为向下相交,第二个交点为向上

相交。一般反映为洗盘拉升的特征。

Examples:

>>> f = np.array([ 3 * i ** 2 - 20 * i + 2 for i in range(10)])

>>> g = np.array([ i - 5 for i in range(10)])

>>> flag, indices = vcross(f, g)

>>> assert flag is True

>>> assert indices[0] == 0

>>> assert indices[1] == 6

Args:

f: first sequence

g: the second sequence

Returns:

(flag, indices), 其中flag取值为True时,存在vcross,indices为交点的索引。

"""

indices = np.argwhere(np.diff(np.sign(f - g))).flatten()

if len(indices) == 2:

idx0, idx1 = indices

if f[idx0] > g[idx0] and f[idx1] < g[idx1]:

return True, (idx0, idx1)

return False, (None, None)